IRS Updates to Publication 5708 and Written Information Security Plan (WISP)

In this video we discuss the newly updated Publication 5708, Creating a Written Information Security Plan for your Tax & Accounting Practice. Bellator Cyber Guard is here to empower you with the knowledge and tools needed to stay ahead of cyber threats. Subscribe now for regular updates on cybersecurity tools and best practices! Find out how you can protect yourself from Ransomware with Ransomware Rollback® at BellatorCyber.com

IRS Dirty Dozen:

The IRS’s “Dirty Dozen” is an annual compilation of the year’s most prevalent tax scams, designed to alert taxpayers to fraudulent schemes that can occur at any time. These scams often intensify during tax season, as individuals prepare their returns or seek assistance. The 2024 list includes deceptive tactics such as phishing and smishing attacks, fraudulent Employee Retention Credit claims, and misleading offers to set up online accounts. Staying informed about these scams is crucial to protect your personal and financial information.

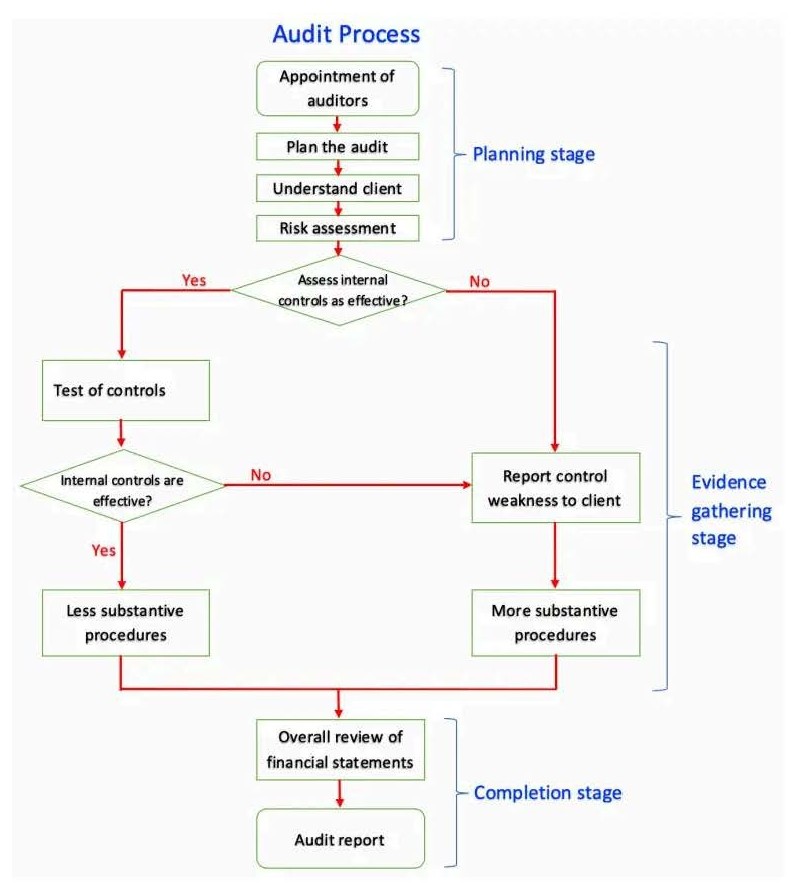

Our Audit Process

At Barrmytaxes, we follow a thorough and transparent audit process to ensure our clients receive the most accurate and effective zero-tax strategies. Our process begins with a detailed review of your financial situation, identifying areas where you can minimize tax liabilities. We work closely with you to understand your specific needs and goals, crafting a tailored plan that aligns with your unique circumstances. Our team uses the latest tools and strategies to navigate complex tax laws, providing you with clear and actionable insights every step of the way. With Barrmytaxes, you can trust that your audit process will be handled with professionalism and precision, helping you secure maximum savings.

Tax Resources

At Barr Advanced Tax Solutions, we understand that these strategies, while

potentially lucrative, can also be a source of tax stress and unexpected liabilities for high-income W-2 earners. They promise tax simplicity but deliver complexity, offer wealth but can create tax-related cash crunches.

Instead of relying solely on these company-provided strategies, we work with you to develop a comprehensive approach that truly optimizes your overall tax picture. We look beyond these corporate offerings to find innovative tax strategies that put you in control of your financial future, rather than leaving it at the mercy of your employer’s stock price and the complexities of equity compensation taxation.

Don’t let the allure of stock-based compensation or conventional tax strategies obscure their potential pitfalls or limit your tax-saving potential. At Barr Advanced Tax Solutions, we go beyond surface-level approaches. Let us show you how to navigate the complexities of equity compensation while implementing our innovative, personalized tax-saving strategies. Our approach not only aligns with your long-term financial goals but also transforms your financial landscape, providing the substantial tax savings you truly deserve. With our expertise, you can maximize the benefits of your compensation package while minimizing your tax burden, creating a powerful synergy that propels your financial success to new heights.

Tax Organizer Forms

Limitations of Common Tax Strategies for High-Income W-2 Earners

At Barr Advanced Tax Solutions, we understand the unique challenges faced by high-income W-2 earners. While many tax professionals offer seemingly attractive strategies, these often fall short for our sophisticated clients. Let’s examine why:

401(k), 403(b), and 457(b) Plans

- Limitation:

- $22,500 contribution limit ($30,000 if age 50+)

- Pain Point:

- For high earners, this barely dents your tax liability. It's like trying to bail out the ocean with a teaspoon.

Traditional and Roth IRAs

- Limitation:

- $6,500 contribution limit ($7,500 if age 50+), with income phase-outs

- Pain Point:

- Many high earners are completely phased out, rendering this strategy useless. It's a locked door with no key.

Health Savings Account (HSA)

- Limitation:

- $3,850 for individuals, $7,750 for families

- Pain Point:

- These minuscule limits are a drop in the bucket for high-income earners. It's like being offered a piggy bank when you need a vault.

Charitable Contributions

- Limitation:

- Generally limited to 60% of AGI for cash donations

- Pain Point:

- Your generosity is capped, potentially leaving significant tax savings on the table. It's frustrating to see your philanthropy limited by arbitrary rules.

Employee Stock Purchase Plans (ESPPs)

- Limitation:

- $25,000 annual purchase limit

- Pain Point:

- For high earners, this limit restricts the potential tax benefits. It's like being allowed only a small slice of a large pie.

Restricted Stock Units (RSUs) and Stock Options

- Limitation:

- Taxed as ordinary income upon vesting or exercise

- Pain Point:

- Can lead to significant tax bills at inopportune times, potentially forcing you to sell shares to cover taxes. It's a tax trap disguised as a benefit.

Deferred Compensation Plans

- Limitation:

- Complex rules, potential forfeiture of benefits

- Pain Point:

- While they offer tax deferral, they come with significant risks and restrictions. It's like being offered a parachute with strings attached - literally.

Home Office Deduction

- Limitation:

- Must be used exclusively for business, deduction limited to income derived from its use

- Pain Point:

- For high-income W-2 earners, this deduction is often negligible and may invite scrutiny. It's like inviting an audit for pocket change.

Mortgage Interest Deduction

- Limitation:

- Limited to interest on $750,000 of qualified residence loans

- Pain Point:

- For high-income earners in expensive real estate markets, this cap significantly reduces the benefit. It's like having a umbrella that only covers your head in a downpour.

These strategies, while touted by many tax professionals, often leave high-income W-2 earners feeling frustrated and underserved. They require significant effort to implement and manage, yet provide minimal impact on overall tax liability. It’s like being promised a feast but receiving mere crumbs.

At Barr Advanced Tax Solutions, we recognize the inadequacy of these conventional approaches for our high-income clients. That’s why we’ve developed advanced, tailored strategies that leverage recent tax legislation to create truly impactful tax-saving opportunities.

Navigating the Tax Maze: Employee Incentive Corporate Stock Strategies

At Barr Advanced Tax Solutions, we often encounter high-income W-2 earners grappling with the complexities of employee incentive corporate stock strategies. While these can appear attractive initially, they frequently present significant tax challenges. Let’s examine these common offerings:

Restricted Stock Units (RSUs)

- Taxation:

- $22,500 contribution limit ($30,000 if age 50+)

- Tax Challenge:

- For high earners, this barely dents your tax liability. It's like trying to bail out the ocean with a teaspoon.

Incentive Stock Options (ISOs)

- Taxation:

- No tax at grant or exercise, but subject to Alternative Minimum Tax (AMT)

- Tax Challenge:

- The AMT trap can result in taxes on "phantom income" if the stock price drops after exercise. It's equivalent to being taxed on money you never actually received.

Non-Qualified Stock Options (NQSOs)

- Taxation:

- Taxed as ordinary income upon exercise

- Tax Challenge:

- Exercise creates a tax liability even if you don't sell the shares. You might end up owing taxes on stock you can't easily liquidate. It's akin to being forced to pay for a meal you haven't consumed yet.

Employee Stock Purchase Plans (ESPPs)

- Limitation:

- Typically limited to 15% of salary or $25,000 annually, whichever is lower

- Tax Challenge:

- For high earners, this cap severely limits the potential tax benefit. It's like being offered a tax deduction, but only on a minuscule portion of your income.

Employee Stock Ownership Plans (ESOPs)

- Limitation:

- Lack of diversification, as your retirement savings are tied to your employer's stock

- Tax Challenge:

- While offering potential tax benefits, it puts both your current income and retirement at risk if the company struggles. It's like putting all your tax-advantaged eggs in one precarious basket.

Performance Shares

- Taxation:

- Taxed as ordinary income upon vesting, which occurs only if performance goals are met

- Tax Challenge:

- You have little control over whether you receive the shares, but when you do, you're faced with a potentially large tax bill. It's like being in a tax game where you don't know the rules, but you're penalized for winning.

Stock Appreciation Rights (SARs)

- Taxation:

- Taxed as ordinary income when exercised

- Tax Challenge:

- Often settled in cash, creating a sudden taxable event without providing actual stock ownership. It's like being promised a slice of the tax-saving pie, but receiving a hefty tax bill instead.

- These strategies often create more tax complications than they solve for high-income earners:

Concentration Risk

They further intertwine your tax situation with your employer’s financial performance.

Timing Dilemmas

You’re compelled to make critical decisions about exercising options or selling shares based on tax implications rather than investment merit.

Cash Flow Hurdles

These strategies can generate large, unexpected tax bills, forcing you to scramble for liquidity at inopportune times.

Complexity

Managing these benefits often requires sophisticated tax modeling and constant attention, consuming your valuable time and energy.

Golden Handcuffs

They can tie you to your employer even when it might be more tax-efficient to explore other opportunities.

Address

Your Success Partner!

Zak Shaik WMS, IAR, CAPP, CWPP

950 E.State Hwy 114

Ste 160

Southlake, TX 76092

Get In Touch

Telephone: (469)702-8955

Email: taxprep@barrmytaxes.com